Chapter 5: Scenario planning in 2025 - In the grip of uncertainty

The last decade has seen the world leave behind a long era of relative stability in which the challenges thrown at the insurance industry and its clients could be readily identified, defined and managed.

It was an era when the big issues, such as climate change, technological advances and regulatory pressures, were met with a high degree of confidence derived from a sense of common purpose and willingness to share knowledge in order to deliver the solutions and resilience needed to meet the challenges.

That has all gone.

We are now all operating outside the previous boundaries of our experience, buffeted by forces we cannot predict, let alone control or influence. It is an era of dramatic Critical Uncertainties. Once the challenge was to address uncertainties that might have seemed just remote possibilities; now we must go further and think the unthinkable.

Scenario planning in 2020

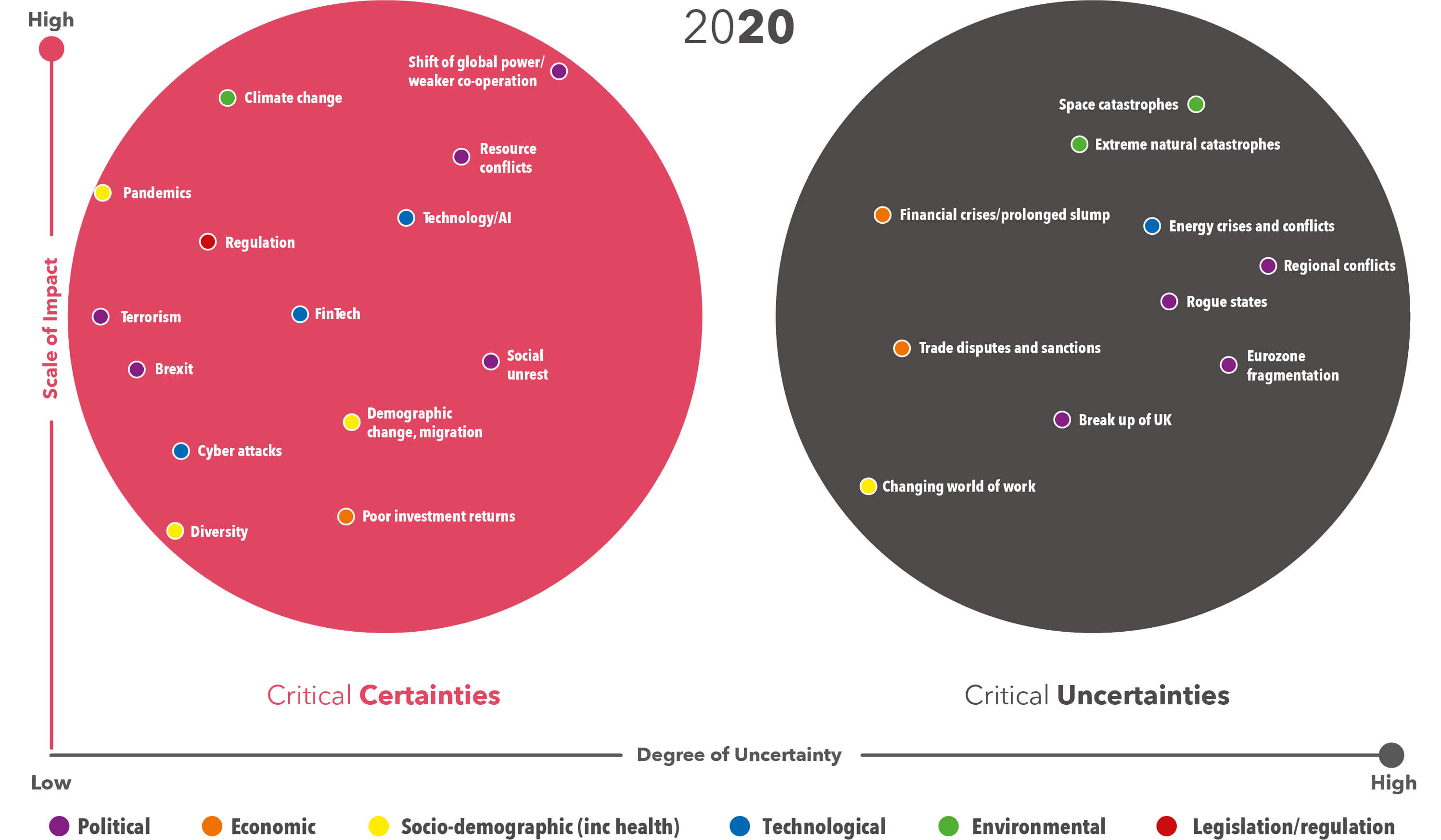

Five years ago, we developed an approach to scenario planning that took us beyond the predictable and obvious and asked challenging questions about what might be unexpected, disruptive and unpredictable in its extent and impact (see fig 1). This took us into a world of Critical Certainties and Critical Uncertainties, with many of the latter barely on the radar of the average boardroom.

In 2020 we found ourselves facing the sobering reality of one of those Critical Uncertainties previously pushed to the fringes of boardroom consciousness – a global pandemic.

“When we first launched our analytical approach to mapping risks we were in the first wave of COVID-19. This made people realise that risks that had been seen as remote and unlikely, often almost dismissed, could become reality and be very disruptive. We are now in a position where uncertainty is the norm and ignoring the outliers on any risk mapping exercise is unwise,” says Helen Faulkner, Head of Insurance at DAC Beachcroft.

The experience of the pandemic was a sharp reminder of the consequences of not mapping Critical Uncertainties into business planning. The insurance industry and its clients are still dealing with this fall out today, says Liam O’Connell, Head of DAC Beachcroft’s Global London insurance practice:

“Event cancellation and non-appearance insurance was, prior to COVID-19, probably five to 10 percent of my workload. Suddenly it became 100% as every event in the entire world got cancelled.”

Scenario planning in 2025

Over the last five years, many other highly disruptive risks, once viewed as remote possibilities, have also forced their way centre stage as Critical Certainties, including:

· war in Europe

· unparalleled trade disputes and sanctions regimes

· energy crises

· the collapse of the western consensus on economic inter-dependence and security

· the growth of populism, and

· the role of artificial intelligence.

Other issues have moved the other way: they have become Critically Uncertain but must not be forgotten or ignored, says O’Connell, citing the pandemic risk.

“Some of the expert work we are seeing from epidemiologists and the like leaves you cold as to the likelihood of another much worse pandemic with an even more catastrophic impact.”

A further dimension is the pace of change. The triggers are manifold, some driven by political forces, others by natural catastrophes.

“There is a relentless acceleration of major events that suddenly brings Critical Uncertainties into sharper focus, moving them across the scenario planning spectrum and demanding that they are addressed as highly disruptive Critical Certainties. Mapping these factors is not a ‘once and done’ exercise. It requires constant review to ensure that key resources are deployed and policy decisions made quickly,” says Faulkner.

All of this sits in a very changed geopolitical context, once little discussed in the corridors of power in the insurance industry but now impossible to hide from, says José María Álvarez-Cienfuegos, a DAC Beachcroft Partner based in Madrid:

“We are in the middle of a storm, which is likely to continue moving and changing. In Europe we have gone through a lot of changes of governments, from extreme to extreme. Obviously, you expect changes in governments in different countries. But historically, the changes were not as significant as they are nowadays. Traditionally, you get countries being governed for ages from centre parties with a bias to the right or to the left. Now we switch from extreme right wing parties to extreme left wing governments. This swinging from extreme to extreme brings huge changes in terms of regulations and public policies, impacting companies and the insurance industry.”

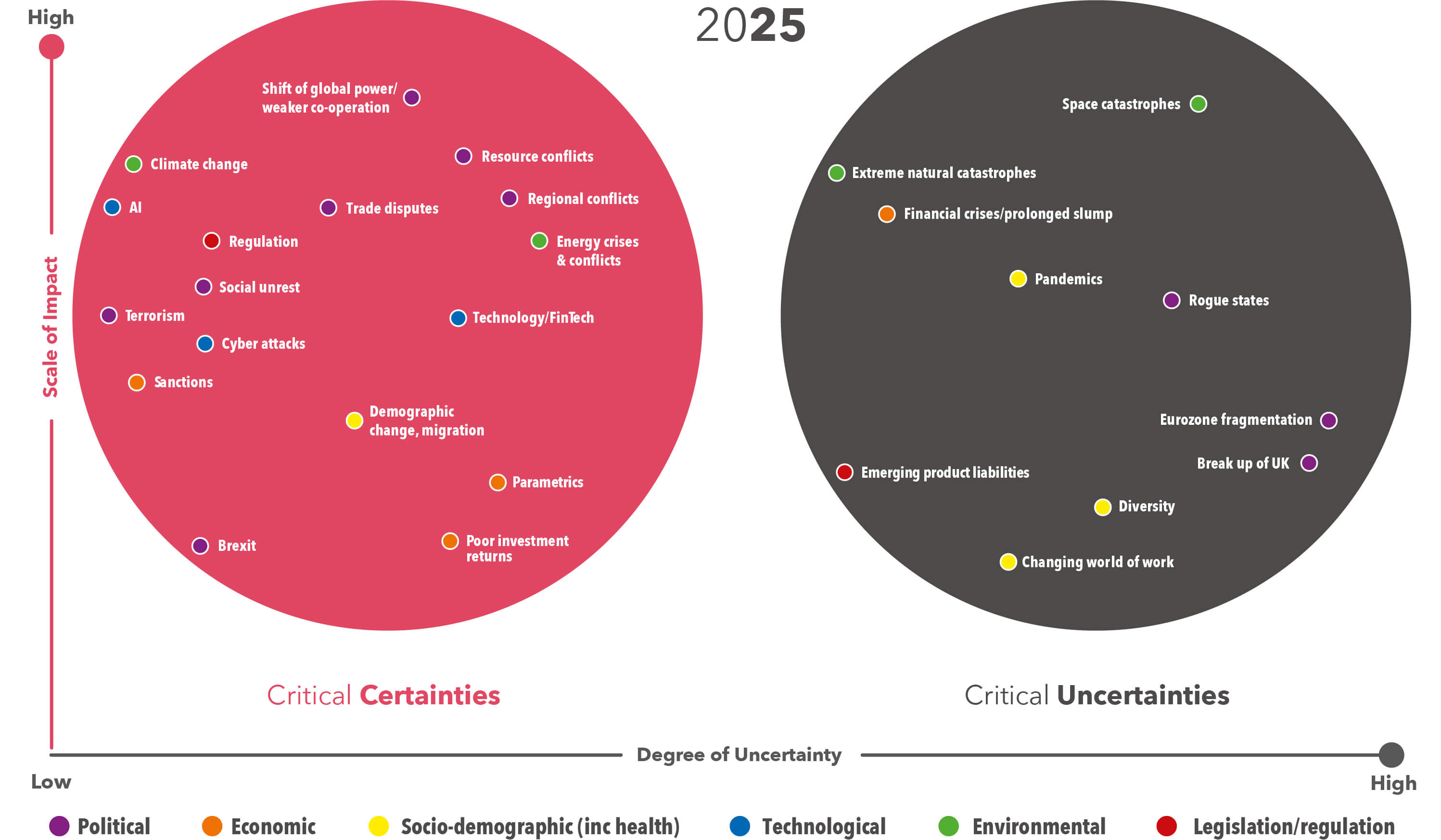

Using our scenario planning methodology we have reassessed the detailed maps of Critical Certainties and Critical Uncertainties and their often complex interconnectivity (see fig 2).

Fig 1: Mapping critical certainties and uncertainties in 2020

The core concepts of our analysis are derived from the scenario planning methodology we used in 2020.

Critical Certainties are those events where we know something will happen that will be disruptive and which businesses must take into account in their business strategy and operational planning. It might not, at this stage, always be clear precisely what those impacts might be. Critical Uncertainties are those events that might happen and if they do could be very disruptive.

Fig 2: Mapping critical certainties and uncertainties in 2025

Mapping in 2025 shows significant movement across the spectrum, both as to the degree of uncertainty and scale of impact, with many topics moving from one sphere to the other.

There are some big movers and new players, set out below.

War in Europe and regional conflicts

Five years ago, the tensions between Russia and Ukraine were simmering in the background. Crimea had been seized in 2014 and fighting in the eastern Donbas seemed to be contained. It was mapped as highly uncertain and of moderate potential impact.

Now, it is centre stage, a Critical Certainty. It is not ending anytime soon and threatens to escalate further with the UK and Europe racking up defence spending, talk of Russia using tactical nuclear weapons and America apparently stepping back from its post-war commitments to ensure the freedom of western Europe.

No-one knows where this will end, especially with two wildly unpredictable leaders – Donald Trump and Vladimir Putin – as the key protagonists.

“When Putin looks at Trump, he’s looking in the mirror into the eyes of somebody else completely unpredictable and maybe that maintains an equilibrium of chaos on the world stage,” says O’Connell.

There is also a powerful connectivity between many of the issues, most obviously the link between energy crises and conflicts, says Larry Klein, DAC Beachcroft Partner and Location Head in the USA:

“There have always been some geopolitical tensions, but most of them were contained. They weren't particularly disruptive because they didn't spread out. The Russian-Ukraine conflict is not contained because it has huge implications for energy markets. It also has huge implications for the way Europe arms itself and views future potential threats from Russia. It's not contained in the way that some of the conflicts that were present 10 years ago were.”

The sharp focus on Russia’s invasion of Ukraine must not detract the attention of the world’s insurers from other simmering conflicts. The conflict between Israel and Hamas in Gaza has already highlighted the continuing instability in the Middle East. This was exacerbated in June with Israel's attacks on Iran and subsequent retaliatory attacks on Israeli cities. The sudden US intervention showed just how quickly conflicts can escalate in this region. The threats from the Iranian regime included a warning that it could close the Strait of Hormuz, which would have a major impact on oil prices and shipping, with all that implies. The pull-back from the brink of an all-out conflict across the region involving the US has a fragility about it which should make any business with interests in the region very nervous.

This volatility does not just surround the Middle East. Mainland China's determination for reunification, coupled with the pro-independence stance adopted by the current authorities in Taiwan, has heightened the risk of escalation. This is a major concern as it has similarly wide implications, says Klein:

“It would be the same if a conflict breaks out across the Taiwan Strait. That wouldn't be contained. It would have a huge impact on world trade, because so much world trade goes through the South China Sea.”

The unpredictability of how the United States might react, with President Trump showing that his election promise not to intervene in foreign conflicts is easily discarded, perfectly illustrates just how deep the scope of the uncertainties lie:

“We don't know what the Trump administration would do - it's so unpredictable. There was a time when the United States would definitely intervene. Then you would have a U.S.-China conflict, which would be horrible, but no-one knows if that would happen now.”

Regional conflicts now sit firmly as a highly disruptive Critical Certainty with a network of connections pulling in Energy crises, Sanctions, Shift of global power/weaker co-operation, Terrorism (including cyber terrorism) and Poor investment returns. No-one can be certain where these major regional conflicts might lead.

Trade disputes and sanctions

It no longer seems manageable to bracket trade disputes and sanctions together. In the last five years both have grown in scale and impact, with a wide range of consequences for insurers.

Alongside America’s weakening commitment to western, and especially European, security, international trade is probably the field that most vividly illustrates the realignment and breakdown of the post-war settlement.

Both were enshrined in the Atlantic Charter signed by Winston Churchill and Franklin D Roosevelt in 1941. It was a powerful commitment to peace and security but also laid the foundations for the creation of the post-war multilateral economic system. It set out the need for “the fullest collaboration between all nations in the economic field …to further the enjoyment by all States, great or small, victor or vanquished, of access, on equal terms to the trade … of the world which [is] needed for their economic prosperity.”

This led to the establishment of the General Agreement on Tariffs and Trade in 1948 and, ultimately, to the founding of the World Trade Organisation (WTO) in 1995, underpinning the then emerging era of globalisation.

President Trump’s tariff wars have completely undermined that system. America nominally remains a member of the WTO but has not made any contributions for 2024 or 2025. It is the subject of a barrage of complaints to the WTO, led by China.

Nothing better encapsulates the way the Trump administration wraps uncertainty around uncertainty than its approach to tariffs, says Paul Baker, Partner and political risk, political violence and trade credit lead at DAC Beachcroft:

“The use of tariffs appears inconsistent in approach. Initially, the methodology adopted was vaunted as a complicated criterion, looking at a variety of factors. In fact, it was simply based on effective trade flows: what comes in, what comes out, apply 10% to everyone and extra in the event the US was in a trade deficit.”

The tariff wars were launched by President Trump with some tough language about how they were here to stay. Within a little over a week, however, things started to change:

“It appears that in an environment where bond markets started getting a bit shaky, things changed suddenly for the majority of nations, although China remained a significant outlier."

“China and the US then, for a while, remained in a period of mutual escalation, culminating in, effectively, a trade embargo on both sides.”

At the time of writing, there appears to be a de-escalation between the two superpowers, with it being difficult to ascertain if one party blinked first or if both felt it in the mutual interest to pull back.

According to Baker, that vacuum of knowledge associated with tariffs and beyond presents businesses and their insurers, especially those in the political risks and trade credit markets, with some crippling dilemmas:

“When you're in a scenario where you have an unpredictable state actor with that much power, it is incredibly difficult for private companies, their financiers and insurers to make decisions in the context of future decisions."

“But in circumstances where insurers and their clients may already have three or five year policies in place that commenced before the Trump administration came in, one might be quite worried as an underwriter or a claims handler or an actuary as to the direction of travel. How do you reserve as an actuarial function within an insurance company when it's incredibly difficult to predict where the geopolitical winds are going to move?”

Sanctions, too, have increased in focus, with those on Russia in the immediate past not bringing about the resolution in Ukraine the West may have hoped for, says Baker.

“Sanctions are an effective tool if the entire world is united behind them. What you have now compared, for example, to the days of the first Iraq war and Saddam Hussein, is a very fractured world with different spheres of influence. Of these multiple spheres, arguably one sees a Chinese sphere of influence, a US sphere of influence, and somewhere in the middle the European Union trying to navigate a way through. For example, if the UK and Europe extend sanctions on Russia, one might query their impact if China, India, and the US etc. don't follow suit.”

Technology and AI

Since the 1980s, the impact and pace of technological change has been a hard-wired certainty as a driver of change in the world of business. In our previous mapping exercise, we started to highlight the likely impact of artificial intelligence but within an overall consideration of the evolution of technology. However, we now have to look at AI with a clearer focus on its wide-ranging and disruptive impact.

Views on the rapid rise of AI use in every day life vary wildly from utopian to dystopian. It is important to maintain a balanced view with a clear grip on the business implications and not get distracted by the more extreme visions of where AI might take the world, says Jade Kowalski, Partner and data, privacy and cyber lead at DAC Beachcroft in London:

“Moving on from the hype of last year, the insurance industry is executing well thought out, impactful AI-enabled initiatives, taking time to ensure that they are delivering on articulated objectives and value propositions that add to the firm's offering."

Specialist teams are being pulled together, using existing and new skills:

“Many insurers are expanding existing resources and, in some cases, creating entirely new teams. Data scientists are in demand. Multi-disciplinary teams are very much needed to ensure AI systems are developed and used in compliance with legal and regulatory obligations,” says Kowalski.

The creation of such teams is enabling insurers to explore the latest developments, such as agentic AI, a type of artificial intelligence where systems can make decisions and perform tasks autonomously, without requiring human intervention. However, leaving aside legal and regulatory risk, there are many other factors to consider when assessing new AI-enabled initiatives. The use of human knowledge, skill and empathy is crucial.

"Ultimately, the insurance industry supports in moments of crisis, often in the policyholder's darkest hour. That is true from the smallest consumer policy to the largest corporate policy; from the property claim arising from a leaky pipe to the global retailer suffering a ransomware attack. Ensuring that the use of AI systems enhances, rather than detracts, from the policyholder experience is key," says Kowalski.

New uncertainties

Reassessing the mapping of Critical Certainties and Critical Uncertainties is not just a question of looking at what is already on the map and asking whether it deserves greater or lesser prominence.

Asking what’s missing and what is now coming over the horizon that was not visible to us before is essential to ensure the relevance of this type of scenario planning.

Some of those issues, as we have discussed, are already encapsulated in existing topics but have grown in importance – and potential disruptive power – and they merit deeper consideration on their own. But others that may have been twinkling faintly in the far distance just five years ago are now with us in full force.

Among those is the growth of parametric insurance. This has grown in importance as the industry struggles to cope with uncertainty across the scale and scope of risks, geopolitical volatility and the impacts of climate change.

“The parametric tool provides a coverage response to emerging and unknown risks. It is a way for the insurance industry to learn progressively about these risks while still providing a certain coverage because parametric insurance is more predictable than traditional insurance,” says Álvarez-Cienfuegos.

Ultimately, a parametric solution might replace a previous traditional model but this will not always be the case: “Parametric insurance can provide an intermediate level of coverage until the insurance industry is able to offer traditional insurance for certain risks that are emerging”, he says.

Also on the horizon of emerging risks – and thus bringing new uncertainty – are the wide range of issues large groups of claimants are now pursuing and which could trigger unexpected judgments leading to enormous settlements. There are plenty of candidates for this, including forever chemicals (PFAS), weight loss drugs (semaglutides), hair straightening chemicals and even Ultra Processed Food. Following the lead of a significant action in the US, a representative action is also underway in Italy relating to defective CPAP sleep and respiratory care devices, highlighting the risk of product-related actions.

It is also impossible to ignore the growing focus on mental health, often linked to the alleged damaging impacts of social media. This is an issue that is going to catch up with the tech giants but will also grow in importance for insurance firms as employers.

ESG backlash

A common thread running through many of the issues we have covered is the huge uncertainty caused by political change, more volatile now in every continent than any time since the Second World War. This is vividly encapsulated in how the industry is having to respond to ESG issues. As Simon Konsta, a professional and financial lines Partner at DAC Beachcroft in London, recently commented in a separate thought leadership piece on Informed Insurance:

“Over the last year, the consequences of ongoing economic challenges and geopolitical events have ushered in what has been called a "rollback" in ESG – a renewed and altered focus on policies intended to combat climate change and the pursuit of equity, diversity and inclusion (EDI). The implications of this backlash are pertinent to corporates across western economies, with the potential to impact corporate strategies, investment paths and engagement with stakeholders from shareholders to consumers.”

The concerted attack on diversity policies by the Trump administration, despite the different legal and regulatory backdrop to positive discrimination in the United States, has thrown diversity policies into the melting pot alongside ESG.

In 2020, most firms knew what diversity and inclusion meant and where it sat in their corporate priorities: it was a Critical Certainty, with a gradual but not disruptive impact across businesses. Now it must be classed as a Critical Uncertainty, especially for firms with strong American connections.

The response to these unpredicted pressures on ESG and EDI policies also poses a dilemma for many firms as they struggle with the need to retain the trust of customers and employees, current and future. Sudden changes to these much publicised policies – which could quickly change back– need to be carefully nuanced to avoid impacting reputation and appearing too capricious as the political winds change direction.

There is some relief

These rising geopolitical pressures are not one-dimensional in their impacts, however. On some fronts they offer relief from the Critical Certainties and Critical Uncertainties that were crowding in on us five years ago.

Brexit loomed very large in the wake of the UK’s referendum that narrowly voted to leave the European Union as the exit route was by no means clear - something with potentially significant implications for the insurance industry. The politics of the Conservative Party meant the option chosen was a so-called hard Brexit but in leaving on those terms, the government introduced a degree of certainty, allowing businesses to plan. Now, the Labour government is working to smooth off some of the rough edges of that hastily agreed deal, creating a calmer, less disruptive relationship with the EU, although the rapid rise of Reform UK injects plenty of uncertainty about what the medium-term might hold.

In the wake of the Brexit referendum, the possibility of the break-up of the UK still loomed large. Scotland had voted to remain in the EU and the Scottish National Party (SNP) was in its pomp. A combination of the decline in the SNP and the widespread realisation that the huge instability around the world creates a greater need for closer co-operation between countries has reduced the likelihood of another independence referendum anytime soon. It has not disappeared as an uncertainty that firms must consider but it seems less pressing as an issue.

Much the same can be said of the threat the Eurozone might break up. It was much talked about in the last decade but now seems unlikely with more countries, such as Bulgaria next January, adopting the Euro. As with some of these other issues the unpredictable rise of populism in Europe could change this very quickly.

Thinking the unthinkable

So many issues, so many trends, so many connections. It is a challenge for businesses to understand them and their implications but by mapping them using a consistent scenario planning methodology, albeit one that inevitably includes an element of subjectivity, we can ensure that we are not leaving ourselves exposed through ignorance or naivety. As we discussed five years ago, through a combination of prudent maturity and imagination, we can build genuine operational and financial resilience, not just a back-up plan to keep the proverbial lights on.

{kind=link}